Never miss a story — sign up for PLANADVISER newsletters to keep up on the latest retirement plan adviser news.

Thought Leadership April 3, 2023

Client Material: Consolidating Retirement Accounts

Advisors: Share this flyer with clients to help them understand the benefits of consolidating their retirement accounts.

Sponsored by MFS Investment Management

The average American worker changes jobs multiple times1, and while a new job often means better pay and benefits, it can also result in a forgotten retirement account. In some cases, depending on your retirement investor’s situation, it might make sense to leave retirement savings in a prior employer’s plan, but consolidating retirement accounts in a new employer’s plan or individual retirement account may lead to better outcomes. Review with your retirement investors these key considerations of consolidation:

Potential risks of leaving a retirement account with a prior employer

Higher Fees Consider the investment and administrative fees assessed by your old employer, new employer and IRAs. If your old employer has higher fees, they could eat into account balances.

Losing Track Multiple accounts can make it hard to understand your total retirement savings and determine if your asset allocation is right for your goals. You can also lose track of them.

Potential Lower Investment Returns2 Plans are allowed to automatically roll over accounts of less than $5,000 into an IRA2, which may not offer the same investment options as your new employer’s 401(k) or offer investments that may provide a lower return.

Cybersecurity Having multiple accounts can increase chances of fraud or theft. Reducing the number of accounts may reduce your exposure.

Potential benefits of leaving a retirement account with a prior employer

Lower Fees Your old employer may have lower fees than your new employer’s plan or an IRA.

Access to Investments While most plans offer a range of funds, you may want to maintain your access to a fund offered by your prior employer.

79% of defined contribution plan participants consider it important to consolidate retirement assets in as few accounts as possible.3

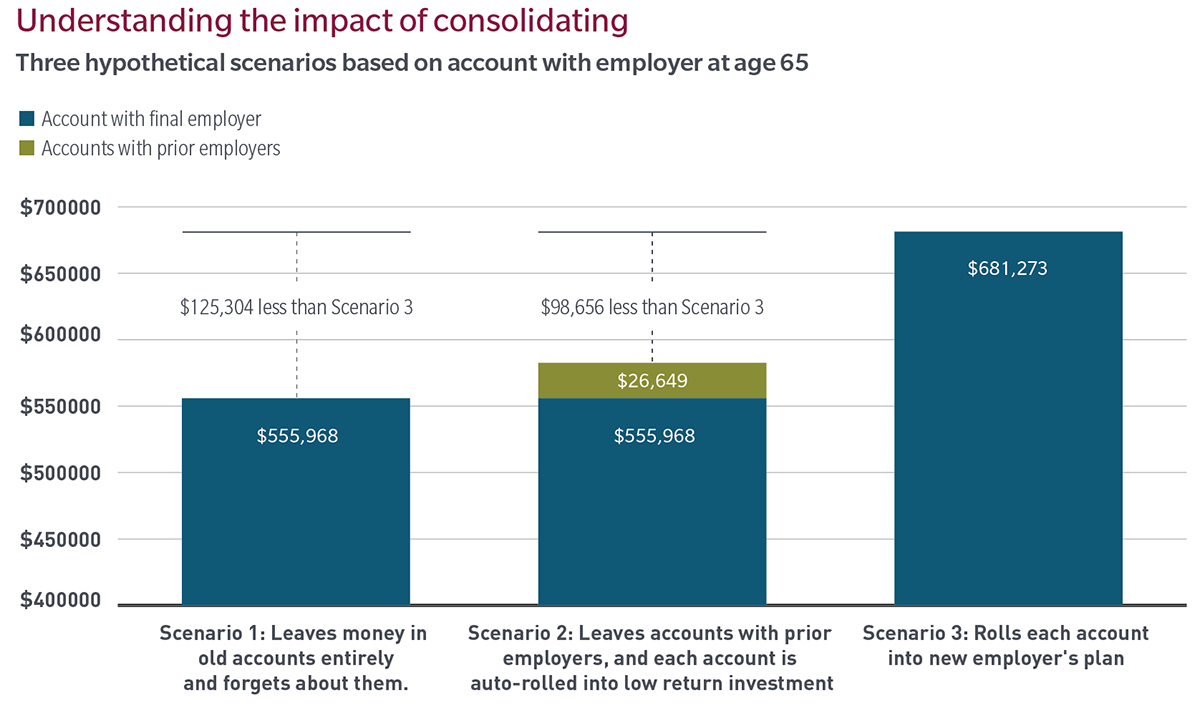

Let’s look at how these potential risks and benefits could play out. Amala starts her career at age 23 and changes jobs every three years. Along the way, she participates in each employer’s 401(k) plan, accumulating a balance in each. At age 35, Amala finds her dream job and is able to save more and benefit from her employer’s company match. She ends up working there for the rest of her career.

By consolidating her four prior 401(k) accounts together, Amala was able to generate a larger balance and keep on track for retirement.

ASSUMPTIONS

■ Age at first job: 23

■ Age of retirement: 65

■ Salary at first job: $40,000

■ Salary increase per year: 2.0%

■ Total employee + employer contribution between ages 23 and 35: 3.0%

■ Total employee + employer contribution after age 35: 9.0%

■ Changes jobs every 3 years between age 23 and 35 (5 employers in total)

■ Return on 401(k) investment: 6.0%

■ Return on low-return2 rollover investment: 1.0%

These hypothetical examples are for illustrative purposes only and are not intended to predict the returns of any investment choices. Rates of return will vary over time, particularly for long-term investments. There is no guarantee the selected rate of return can be achieved. Any investments may have fees and expenses that are not taken into account, which would lower the performance. Regular investing does not ensure a profit or protect against loss in declining markets.

Key takeaway

Your investment professional can help you make an informed decision on whether to leave retirement accounts with prior employers or consolidate them, which can be key to pursuing your retirement goals.

1 Source: Bureau of Labor Statistics, U.S. Department of Labor, The Economics Daily, Median tenure with current employer was 4.1 years in January 2020

2 Source: Internal Revenue Service Notice 2005-5.

3 Source: MFS Global Retirement Survey, US respondents. Q1: How important is it for you to be able to consolidate all retirement assets into one or as few accounts as possible? Percentage represents the sum of respondents that chose somewhat important, very important or extremely important.

Methodology: Dynata, an independent third-party research provider, conducted a study among 1,020 Defined Contribution (DC) plan participants in the US on behalf of MFS. MFS was not identified as the sponsor of the study.

To qualify, DC plan participants had to be ages 18+, employed at least part-time, actively contributing to a 401(k), 403(b), 457, or 401(a). Data weighted to mirror the age / gender distribution of the workforce. The survey was fielded between March 31 and April 13, 2021.

There are advantages and disadvantages to rolling money out of your employer’s plan and into an IRA. You will need to compare such features as investment options, services, fees and expenses, withdrawal options, required minimum distributions, tax treatment and your unique financial needs and retirement goals. Please be aware that rolling over retirement assets into one IRA account could potentially increase fees as the underlying funds may be subject to sales loads, higher management fees, 12b-1 fees, and IRA account fees such as custodial fees. For assistance in determining if a rollover to an IRA is appropriate for you, consult your financial advisor or investment professional.

The views expressed are those of MFS and are subject to change at any time. These views are for informational purposes only and should not be relied upon as a recommendation to purchase any security or as a solicitation or investment advice from the Advisor. No forecast can be guaranteed.

MFS does not provide legal, tax, or accounting advice. Individuals should not use or rely upon the information provided herein without first consulting with their tax or legal professional about their particular circumstances. Any statement contained in this communication (including any attachments) concerning US tax matters was not intended or written to be used, and cannot be used, for the purpose of avoiding penalties under the Internal Revenue Code.

MFS FUND DISTRIBUTORS, INC.