Thought Leadership December 12, 2017

Capitalizing on growing and evolving small to mid-market 401(k) plans

Sponsored by AXA

Large market retirement savings plans may seem like an obvious target for investment advisors. However, there is great opportunity in small and mid-market defined contribution (DC) plans, where growth is strong and plans are evolving to look more like their larger counterparts. “The small market space represents the largest share of total assets and plans out there,” says Jim O’Connor, 401(k) National Sales manager and head of Business Development at AXA Retirement Plan Services. “With 98% of plans having less than $25 million in assets, and 58 million Americans not covered by a 401(k) or employer-sponsored plan, there’s a huge opportunity for growth.”¹

Large market retirement savings plans may seem like an obvious target for investment advisors. However, there is great opportunity in small and mid-market defined contribution (DC) plans, where growth is strong and plans are evolving to look more like their larger counterparts. “The small market space represents the largest share of total assets and plans out there,” says Jim O’Connor, 401(k) National Sales manager and head of Business Development at AXA Retirement Plan Services. “With 98% of plans having less than $25 million in assets, and 58 million Americans not covered by a 401(k) or employer-sponsored plan, there’s a huge opportunity for growth.”¹ As this space evolves and plans become more complex, the role of the advisor is more important than ever. Plan sponsors are looking to their advisors to help make the best decisions for their plan and their employees, helping ensure that employees are prepared for retirement. Executives at AXA Retirement Plan Services, part of AXA U.S., a leader in providing financial security and retirement products, point to three key trends that offer advisors new opportunities to grow their business.

• As the defined contribution plan space matures, the institutional mindset of larger plans is moving down market. As a result, small and mid-market plans have a new and growing focus on services, capabilities, and plan design features once afforded primarily to large plans.

• The role of the advisor is evolving to be an extension of the plan sponsor, meaning advisors are redirecting their time and resources to help sponsors monitor plan health and ensure operational effectiveness and efficiencies.

• New developments on the regulatory front, combined with lack of understanding of basic fiduciary responsibilities, have left plan sponsors worried they face heightened risk exposure.

Institutional mindset boosts demand for up-market services and design features

As smaller plan sponsors look to get the same value from their retirement plan providers that larger plan sponsors do, O’Connor sees several key areas of focus:

• Tailoring financial wellness and education programs to both plan sponsor clients and individual plan participants

• Introducing design features such as automatic enrollment and automatic escalation of participant contributions

• Developing investment menus that give participants more choice and more opportunity to diversify, stay on track, and reach their retirement savings goals

• Ongoing benchmarking to show how plans stack up against the competition, so that plan sponsors can better manage their plans and maximize the value of their vendor’s offering

“Investment flexibility is a requirement now, even in the small plan space,” O’Connor says. “Plan sponsors want to be able to choose from a diverse set of investment options so that plan participants can maximize retirement savings, based on their individual risk tolerance, proximity to retirement, and investment style. They’re looking for actively managed funds, passive investments such as index funds, target date and managed allocation funds for those who want to put their plan on auto pilot, as well as institutional share classes that can lower the cost of investing for their participants.”

Business owners are also interested in ways to maximize their personal contributions. Advisors can help with strategies such as cross-tested profit-sharing features, safe harbor plan designs, and, in some cases, cash balance plans that work in tandem with the 401(k). The success of these more sophisticated types of designs will depend on the goals of the business owner, the demographics of the plan, and the budget for contributions.

As small business plan sponsors strive to provide the best plans possible, they are using benchmarking more often and are comparing a wider variety of services. With so many smaller plans in place now, and that number growing, this provides an opportunity for advisors to add value.

“If you aggregate the micro, small and mid-markets together, they account for almost $88 billion of assets under management, through 36,000 401(k) plans,” says Rick Frink, divisional vice president – 401(k). “From a scale standpoint, this is a huge opportunity, especially when you consider that approximately seven percent of those plans are transitioning to new providers every year.”²

Smaller businesses have unique needs that require careful consideration and support. For that reason, benchmarking activities will need to be tailored to each company’s situation. Advisors should consider benchmarking the following:

• Value and cost, to ensure that plans are paying reasonable fees and the value the plan is receiving supports those fees.

• Service and investment, to review the plan’s current vendor and analyze its plan and investments to make sure the sponsor is maximizing the value of the current offering.

• Vendors, to facilitate the transition from one vendor to another, by comparing and contrasting competing vendors. In this way, sponsors can understand how the transition will be handled by the accepting vendor, and identify the one whose offering will best match their needs and provide the most seamless transition.

Advisors are evolving to become an extension of the plan sponsor

“We recognize that in small to mid-market plans, the daily operation of a 401(k) plan is not always the most pressing issue business owners have to deal with,” Frink says. “We recommend that advisors position themselves as an extension of the plan sponsor, providing input, resources, and time on the advisor’s behalf.” This can mean doing things like setting times for enrollment meetings and annual plan reviews, helping to monitor participant deferrals, coordinating targeted enrollment campaigns, and documenting key factors that impact the plan, to ensure it is operating as effectively as possible.

Frink suggests advisors outline the services they will provide in a written services agreement. This document should set realistic expectations for what the advisor will do, and hold each party accountable for what they need to do throughout the course of the year. Those responsibilities may include the following:

Frink suggests advisors outline the services they will provide in a written services agreement. This document should set realistic expectations for what the advisor will do, and hold each party accountable for what they need to do throughout the course of the year. Those responsibilities may include the following: • Setting times for enrollment meetings or annual plan reviews

• Helping monitor participant education, awareness, and enrollment

• Making sure that the plan is operating as effectively as possible

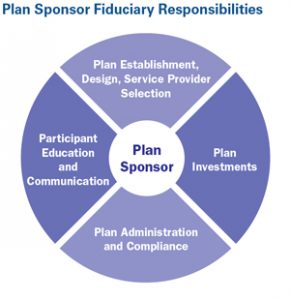

Regulatory changes are heightening plan sponsor concerns about risk

Changes on the regulatory front in the past several years, including requirements on fee transparency and a new rule from the U.S. Department of Labor [DOL] that expands the definition of fiduciary “investment advice” under ERISA [Employee Retirement Income Security Act of 1974], have caused confusion and raised fresh questions from plan sponsors about their fiduciary responsibilities. Some plan sponsors believe they now have new or different responsibilities, when in fact, they’ve been fiduciaries all along. To compound this problem, most small businesses have staff that wear many different hats and lack sufficient time to devote to plan administration and compliance.

This creates an opening for plan advisors to provide education and guidance, along with services that can help plan sponsors meet their responsibilities and properly managing their fiduciary risks.

“Smaller plan sponsors need help understanding and navigating their responsibilities,” says Tina Anstett, JD, director, Advanced Markets – 401(k). “Compared to larger plans, they generally have fewer internal resources who are dedicated to plan oversight or are knowledgeable about the intricacies of defined contribution plans. And unfortunately, many smaller sponsors had their plans ‘sold’ to them years ago and have not made changes to the plan, even though their needs have evolved. Advisors have a tremendous opportunity to educate sponsors about their fiduciary responsibilities and improve plan designs, so that they meet the needs of participants and establish a strong governance structure to ensure compliance.”

How advisors can maximize success with small and mid-market plans

AXA encourages advisors to develop and implement a personal sales and service delivery model that will outline their approach to new business as well as ongoing service. Their model should:

• Identify their value proposition and detail how they will operate in this segment of the market.

• Describe the technologies and resources they will leverage to meet their clients’ needs – upfront and on an ongoing basis. Working with the right vendor will be important, as vendor tools and resources vary and can make a big difference in plan participant outcomes.

• Establish an investment monitoring process for existing plans and an education calendar for participants, and set dates for plan reviews with the sponsor. Plan reviews offer the advisor additional opportunities to add value by providing updates on legislative changes or benchmarking in the marketplace.

“We recognize that advisors, like sponsors, are approaching their workload capacity and need help in making the most of their plans,” says O’Connor. “Technology can help, and we offer a lot of innovative value-adds, including new digital tools that help participants plan for a more comfortable retirement, and product enhancements that strive to fit the needs of smaller businesses. But technology alone isn’t enough. Often, plan sponsors and advisors will need to leverage other resources, such as retirement plan consultants or ERISA attorneys who can meet with sponsors and advisors. We can provide those resources too.”

The service that AXA provides to small and mid-market plans is designed to make administration easier for plan sponsors and outcomes better for plan participants.

For sponsors, AXA Equitable takes care of the heavy lifting by handling the ins and outs of getting a plan set up and running, and keeping it going. This effortless plan management provides the resources required through every step of the plan journey, from plan design through ongoing administration, as well as fiduciary protection from an independent provider. Sponsors will have a dedicated team of professionals to help them from start to finish, and use of a simple, streamlined website and online tools to track the onboarding process and manage the steps they need to take. In addition, their online personal dashboard gives them access to the information they need, including plan participation progress, plan performance, real time notifications and alerts, and access to standard and custom reports, all in one place.

For participants, AXA Equitable provides options for retirement certainty, in the form of investments that can provide guaranteed retirement income, along with personalized retirement planning guidance and an online experience that makes retirement simple, so participants can make meaningful progress toward their goals.

In short, O’Connor suggests that advisors position themselves for success by doing two things: acting as an extension of the plan sponsor, since many sponsors need help in navigating complex compliance and administration issues; and working with a plan provider who has expertise in the marketplace and will be a true partner, keeping the advisor’s and client’s needs in mind.

¹ Department of Labor, Cerulli Associates, PLANSPONSOR.com, 2017 Recordkeeping Survey

² The SPARK Institute, 2016 SPARK Institute Marketplace Update

AXA believes that education is a key step toward addressing your financial goals, and this discussion serves simply as an informational and educational resource rather than investment advice. It does not make a direct or indirect recommendation of any particular product or of the appropriateness of any particular investment-related option. Your unique needs, goals and circumstances require the individualized attention of your financial professional.

AXA Fixed Account is a group fixed annuity issued by AXA Equitable Life Insurance Company (AXA Equitable).

Annuities are long-term products used for retirement purposes. They are contractual agreements in which payment(s) are made to an insurance company, which agrees to pay out an income or a lump sum amount at a later date. Annuities contain certain limitations and restrictions. For costs and complete details, contact a financial professional. All guarantees are based on the claims-paying ability of AXA Equitable Life Insurance Company.

Since 401(k) plans are tax-deferred, annuities used to fund 401(k) plans do not offer any extra tax benefits. Amounts withdrawn may be subject to ordinary income taxes and a withdrawal charge. If amounts are rolled over from another eligible retirement plan, then these amounts may be subject to an additional 10% federal income tax penalty if you later take a distribution before age 59½. Other taxes may also apply; consult your tax advisor.

Mutual funds are subject to market risk, including loss of principal. Please consider the charges, risks, expenses, and investment objectives carefully before purchasing a mutual fund. For a prospectus containing this and other information, please contact a financial professional. Read it carefully before investing or sending money.

The AXA Retirement Plan ServicesSM platform includes recordkeeping, trading and custodial services to plan sponsors for the program. Reliance Trust Company serves as custodian of mutual funds selected by plan participants. PlanConnect, LLC, serves as the platform’s recordkeeper and third-party administrator. AXA Retirement Plan ServicesSM and AXA Retirement 360SM are service marks of the contractual arrangements between affiliated and/or unaffiliated entities within the platform; PlanConnect® is a registered service mark of PlanConnect, LLC (100 Madison Street, Syracuse, NY 13202. (800) 923-6669). AXA Equitable, AXA Distributors, and PlanConnect, LLC are separate but affiliated companies. Reliance Trust Company is a separate and unaffiliated company. The investments in this program are subject to investment risks, including possible loss of the principal invested. They are not insured by the Federal Deposit.

Please be advised that this article is not intended as legal or tax advice. Accordingly, any tax information provided in this article is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer. The tax information was written to support the promotion or marketing of the transactions or matters addressed, and clients should seek advice based on their particular circumstances from an independent tax advisor. Neither AXA Equitable, AXA Advisors nor AXA Distributors provide legal or tax advice.

GE-130226 (11/17) (Exp 11/19)